Bethlehem Steel Corporation

The Rise and Fall of America's Second-Largest Steelmaker, 1857-2003

⤓ Download PDFExecutive Summary -- The Arc of Bethlehem Steel¶

Bethlehem Steel Corporation's 146-year history is the definitive American industrial parable. From a failed iron works founded in the Panic of 1857 to the nation's second-largest steel producer, a Dow Jones Industrial Average component for seven decades, and the builder of some of the most iconic structures in American history -- the Golden Gate Bridge, the Empire State Building, Rockefeller Center -- Bethlehem Steel embodied the rise of American industrial capitalism.1 At its peak, it employed 300,000 workers, built one-fifth of the U.S. Navy's two-ocean fleet, and produced more steel than the entire nation of England.2

Then it went to zero.

The Investment Thesis Across Eras

**1857-1904**: Speculative turnaround -- a regional ironworks pivoting to defense contracts. **1904-1945**: Generational buy -- Schwab's transformation, wide-flange beam monopoly, wartime production dominance. **1945-1970**: Hold/trim -- peak earnings masked strategic complacency and growing labor costs. **1970-1990**: Sell -- structural decline from imports, mini-mills, and technology gaps. **1990-2001**: Distressed -- legacy costs exceeded enterprise value. **2001**: Equity worthless.

The company's destruction was not the result of a single catastrophe but of compounding structural failures over three decades: the refusal to adopt basic oxygen furnaces and continuous casting until a decade after competitors;3 a labor cost structure that reached $26.29/hour (60% above the manufacturing average) locked in by pattern bargaining;4 pension and retiree healthcare obligations that swelled to $7+ billion as the ratio of retirees to active workers reached 10:1;5 and the rise of Japanese, Korean, and domestic mini-mill competitors who produced steel at $50-$100 per ton less.6

On October 15, 2001, Bethlehem Steel filed for Chapter 11 bankruptcy with $4.5 billion in debt. Shareholders received nothing. The PBGC assumed $3.7 billion in unfunded pension liabilities -- the largest single-employer takeover in its history.7 Some 95,000 retirees lost their healthcare benefits entirely. Wilbur Ross's International Steel Group acquired the operating assets for $1.5 billion, shedding all legacy liabilities.8

The contrast with Nucor Corporation tells the story in a single data point: $1 invested in Nucor versus $1 in Bethlehem Steel diverged by over 200x.9

Company Timeline -- Detailed Chronological Milestones¶

Founding Era (1857-1904)¶

| Date | Event |

|---|---|

| April 8, 1857 | Saucona Iron Company incorporated by Augustus Wolle in Bethlehem, PA |

| 1857 | Panic of 1857 halts capitalization; project stalls |

| June 14, 1860 | Company reorganized as Bethlehem Rolling Mills and Iron Company; Asa Packer joins board |

| July 5, 1860 | John Fritz arrives as General Superintendent and Chief Engineer |

| May 1, 1861 | Renamed Bethlehem Iron Company |

| January 4, 1863 | First blast furnace commences operations |

| September 26, 1863 | First railroad rails rolled |

| 1873 | Bessemer steelmaking adopted (nation's 10th Bessemer rail mill) |

| 1875 | Steel rail market share: 5.2% of national output |

| 1879 | Steel rail market share peaks at 11.5% |

| June 28, 1887 | U.S. Navy awards armor plate and forging contracts -- company's strategic pivot |

| 1888-1892 | America's first heavy-forging plant constructed |

| 1893 | Armor plate scandal; $140,485 fine. Ferris wheel axle (89,320 lbs) forged for Chicago World's Fair |

| 1897 | Henry Grey patents wide-flange beam rolling process |

| 1899 | Reorganized as Bethlehem Steel Company by Joseph Wharton and Robert Linderman |

| 1901 | Charles M. Schwab acquires controlling interest (160,000 of 300,000 shares) |

| December 10, 1904 | Bethlehem Steel Corporation incorporated in New Jersey |

The Schwab Era (1904-1939)¶

| Date | Event |

|---|---|

| 1905 | Schwab becomes president and chairman; ingot capacity less than 1% of national total |

| December 1905 | Grey beam mill construction announced ($5 million investment) |

| January 1908 | First wide-flange structural beams produced -- sole U.S. producer until 1927 |

| February 4, 1910 | 9,000 workers strike for 108 days (demands: Sundays off, higher pay) |

| 1913 | Fore River Shipbuilding Company (Quincy, MA) acquired |

| 1914 | WWI begins; Bethlehem has 1.1M-ton capacity, 15,600 employees |

| 1914-1918 | Total wartime earnings: ~$110 million; stock rises from $30 to $600+ |

| 1916 | Eugene Grace named president at age 39; acquisitions of PA Steel and MD Steel |

| April 16, 1918 | Schwab appointed Director General of Emergency Fleet Corporation |

| 1922 | Lackawanna Steel acquired for $60 million |

| 1923 | Midvale Steel & Ordnance and Cambria Steel acquired |

| 1925 | Capacity reaches 8.5 million tons; 60,000+ employees |

| 1927 | U.S. Steel begins rolling "Carnegie Beams," ending Bethlehem's 19-year monopoly |

| 1929 | Grace receives $1.6M bonus (highest-paid U.S. executive); stock market crashes |

| 1931 | McClintic-Marshall acquired ($32M); first quarterly loss since 1909 |

| 1931 | Stockholder lawsuit demands return of $36M in executive bonuses |

| September 18, 1939 | Schwab dies in New York, technically bankrupt (debts exceed assets by $300,000) |

World War II (1939-1945)¶

| Date | Event |

|---|---|

| 1940 | Two Ocean Navy Act drives massive naval contracts |

| February 1941 | Bethlehem-Fairfield Shipyard construction begins in Baltimore |

| August 1941 | SWOC recognized at Bethlehem under federal pressure |

| September 27, 1941 | SS Patrick Henry launched -- first Liberty ship built in the United States |

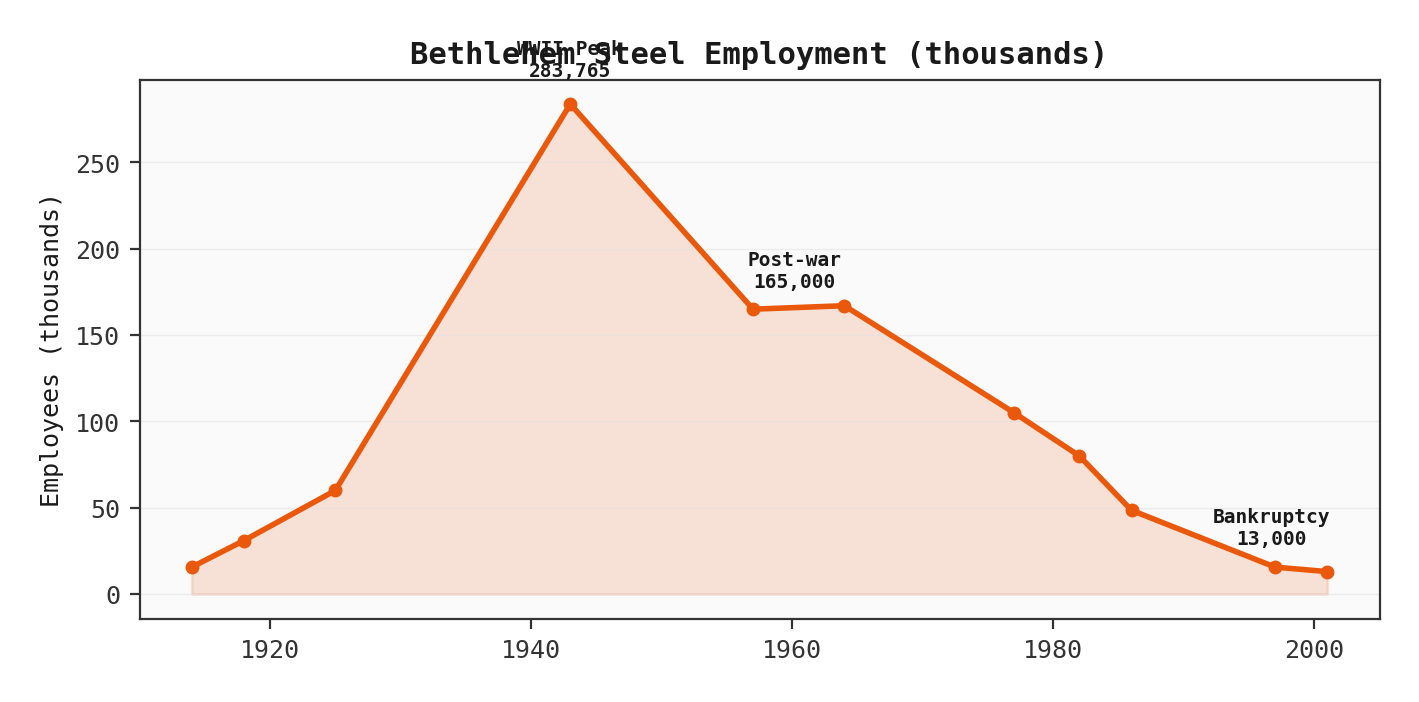

| 1943 | Peak year: 283,765 employees; 380 ships launched; 101% capacity utilization |

| 1940-1945 | 73.4 million tons of steel produced; 1,121 ships built across 15 shipyards |

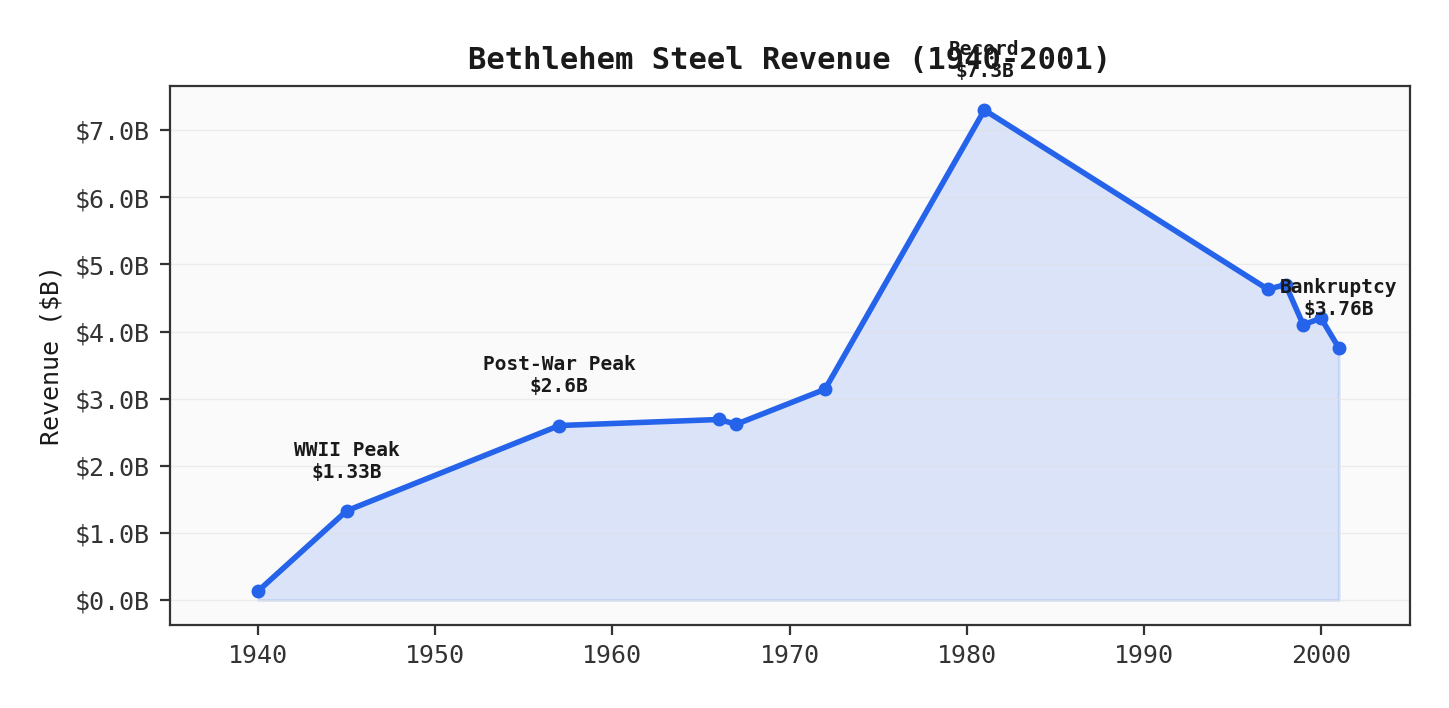

| 1945 | Sales reach $1.33 billion; Bethlehem is nation's largest defense contractor |

Post-War Golden Age (1945-1970)¶

| Date | Event |

|---|---|

| 1955 | Fortune 500 rank: No. 8 (8.2% return on assets) |

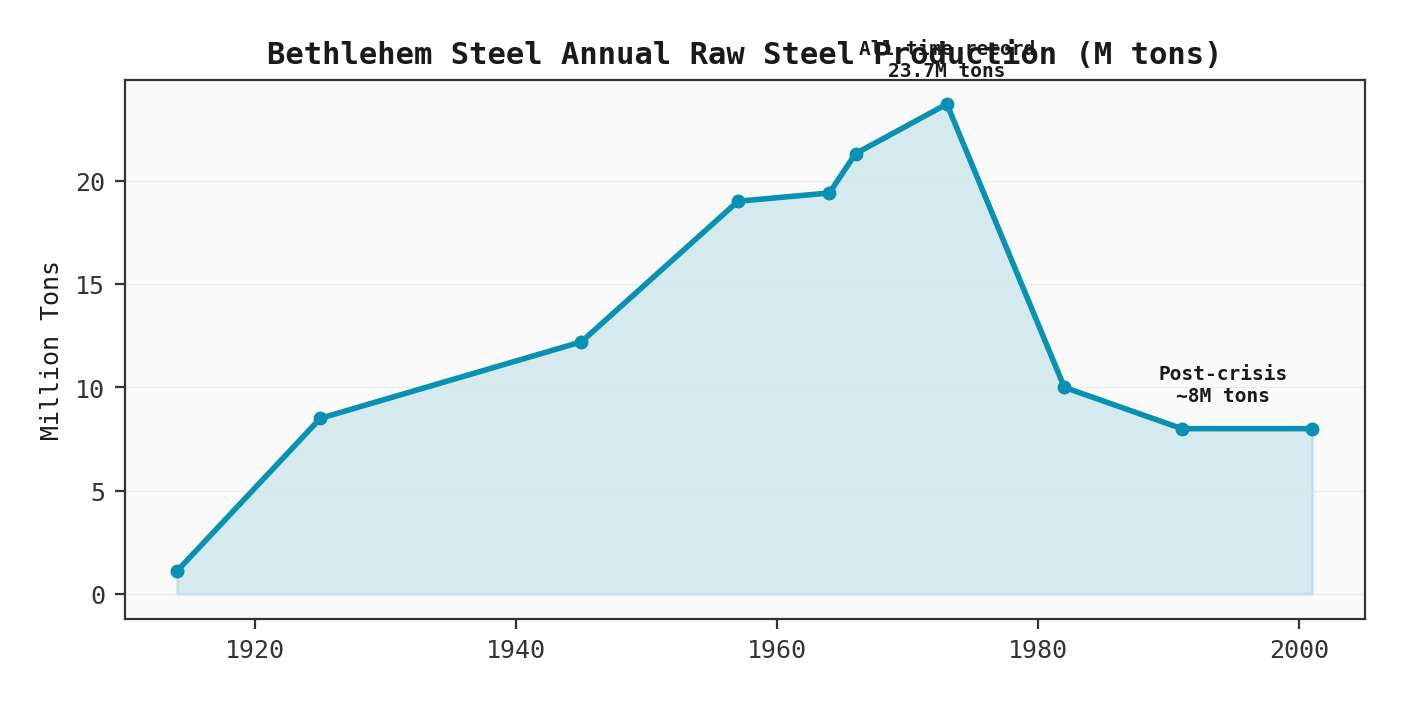

| 1957 | Peak postwar production: 19+ million tons; $2.6B revenue; $190M net income |

| 1957 | Sparrows Point recognized as world's largest steel plant (30,000 employees) |

| 1958 | President Arthur B. Homer is highest-paid U.S. executive ($511,249) |

| July-November 1959 | 116-day steel strike; imports surge from 2M to 5M tons and never recede |

| 1960 | U.S. imports more steel than it exports for the first time |

| 1962-1972 | Burns Harbor plant constructed -- last greenfield integrated steel plant built in U.S. |

| 1964 | First basic oxygen furnaces installed at Lackawanna (a decade late vs. global peers) |

| 1966 | Record output: 21.3 million net tons; revenue $2.69B; net income $170.9M |

| 1967 | Bethlehem loses World Trade Center steel contract |

| Late 1960s | Continuous casting experiment abandoned at 90% completion (~$10M wasted) |

| 1969 | Martin Tower vanity headquarters construction begins ($35M) |

Decline and Crisis (1970-1995)¶

| Date | Event |

|---|---|

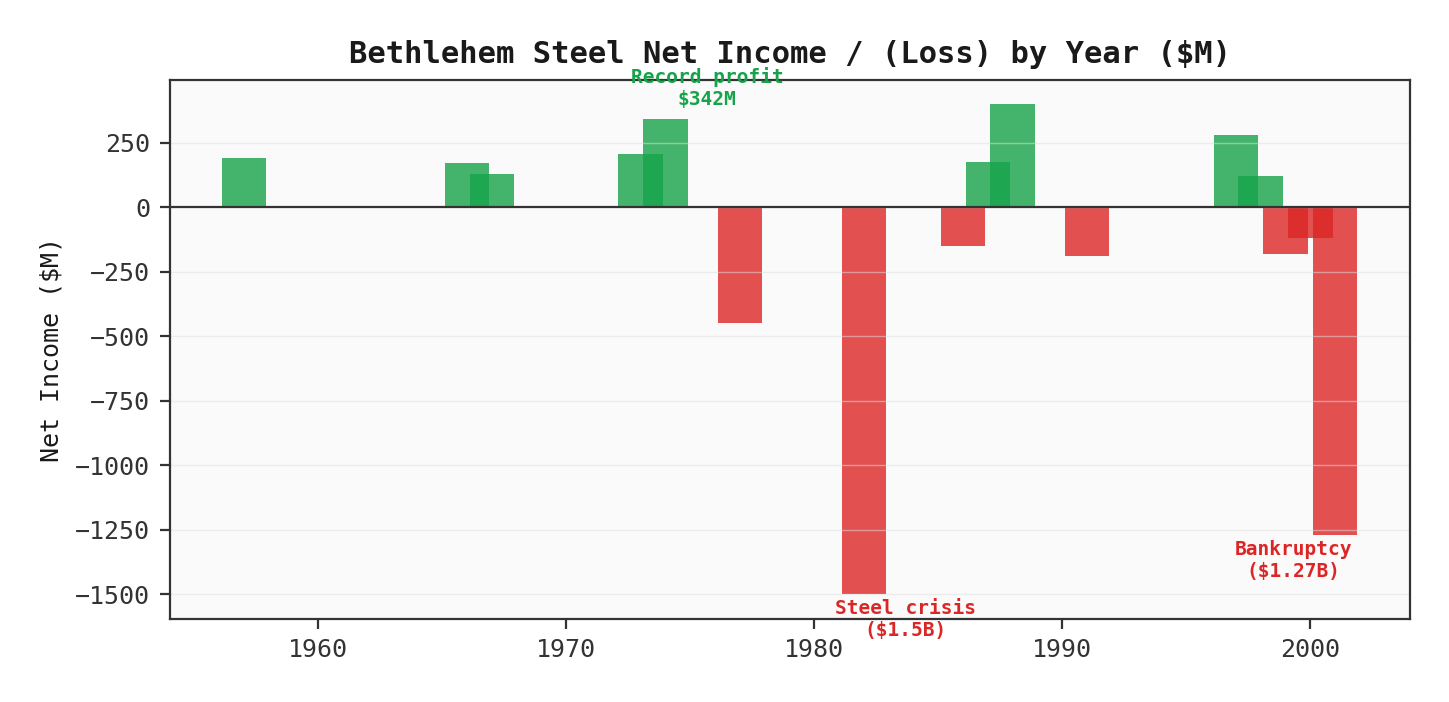

| 1973 | All-time production record: 23.7M tons raw steel; $207M net income |

| 1973 | Experimental Negotiating Agreement (ENA) signed -- 3% annual raises + COLA, no strike |

| 1974 | All-time record net income: $342 million |

| September 30, 1977 | "Black Friday" -- 10,000+ workers laid off in a single day |

| 1977 | First annual loss since 1933: ($448M) |

| 1981 | Record revenue: $7.3 billion; stock 20-year high: $31.75 |

| 1982 | Record loss: ($1.5 billion); capacity utilization falls to 49.5%; Lackawanna closed |

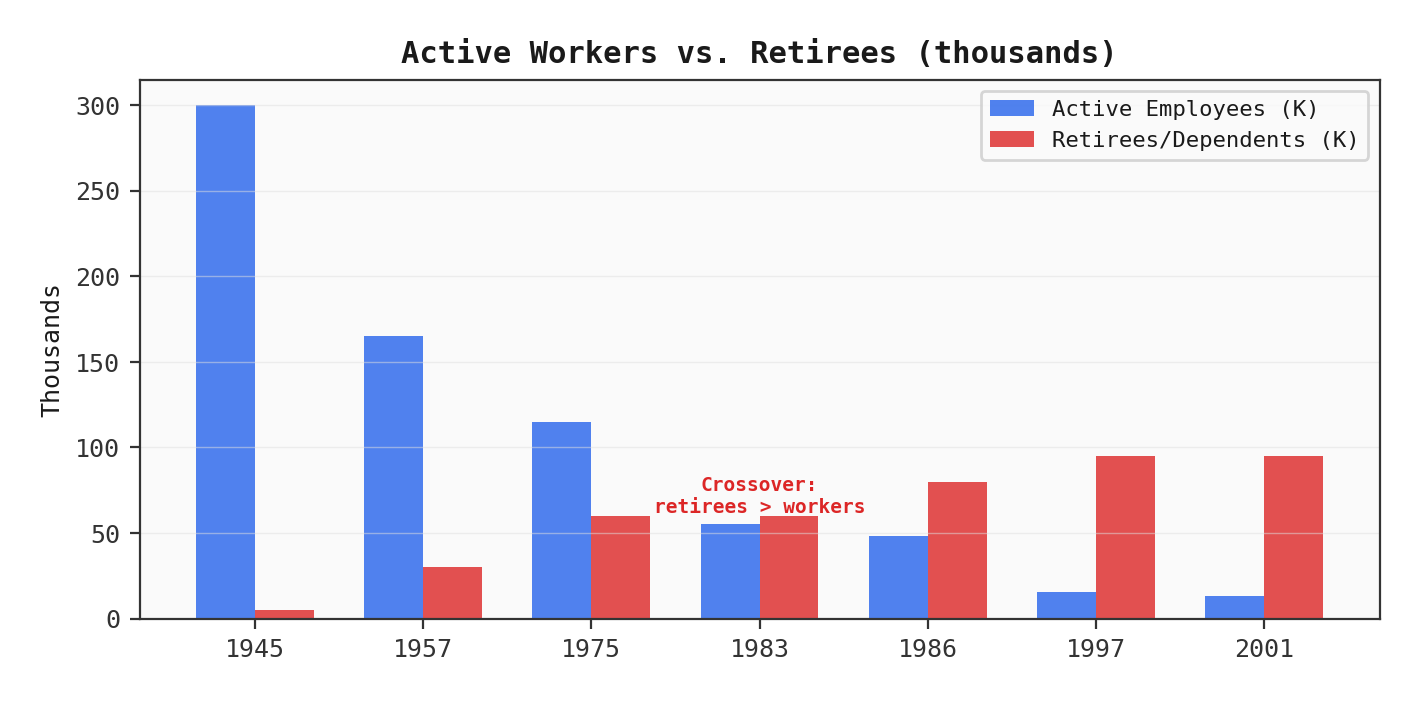

| 1983 | Pensioners outnumber active workers for the first time |

| 1986 | Stock hits all-time low: ~$4 per share |

| 1988 | Brief return to record earnings ($400M+) |

| November 18, 1995 | Last blast furnace cast at Bethlehem, PA plant -- 140 years of steelmaking ends |

Terminal Decline and Bankruptcy (1995-2003)¶

| Date | Event |

|---|---|

| March 17, 1997 | Removed from Dow Jones Industrial Average after 69 years |

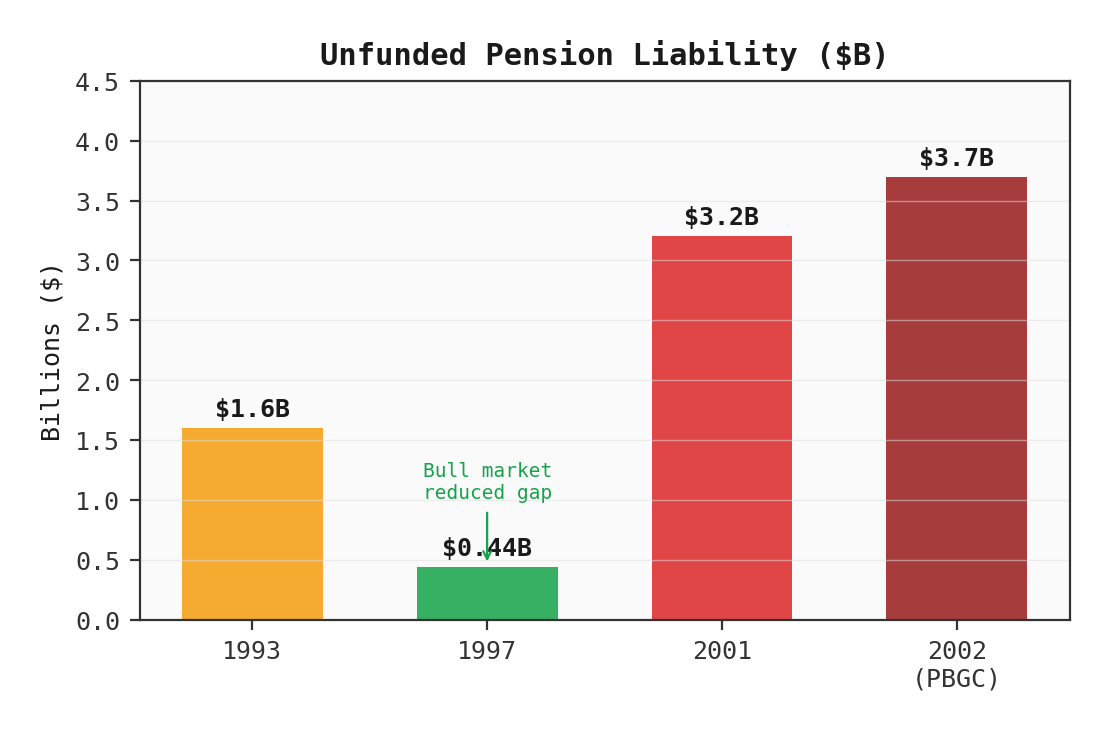

| 1997 | Net income: $280M (last strong year); unfunded pension reduced to $440M |

| May 1998 | Lukens Inc. acquired for $490M + $250M assumed debt |

| 1999 | ($183M) loss; import crisis intensifies |

| 2000 | New $325M cold sheet mill opens at Sparrows Point (one year before bankruptcy) |

| September 11, 2001 | Terrorist attacks accelerate demand collapse |

| October 15, 2001 | Chapter 11 bankruptcy filed; $4.2B assets, $4.5B debt, 13,000 employees |

| June 2002 | Stock delisted from NYSE after 96 years |

| December 2002 | PBGC terminates pension plan ($3.7B underfunded) -- largest takeover in history |

| March 31, 2003 | Healthcare terminated for 95,000 retirees |

| May 7, 2003 | ISG acquisition closes for $1.5B; Bethlehem Steel ceases to exist |

| 2009 | Sands Casino (now Wind Creek Bethlehem) opens on former plant site |

| 2011 | SteelStacks arts and cultural campus opens against preserved blast furnaces |

Founding and Early History (1857-1904) -- From Iron to Steel¶

The company that would become Bethlehem Steel began as the Saucona Iron Company, incorporated on April 8, 1857, by Augustus Wolle, a Moravian merchant who saw the strategic potential of Bethlehem's location at the junction of two railroads near iron ore and anthracite coal deposits.10 The Panic of 1857 immediately stalled the venture.

The enterprise was resurrected in 1860 by Lehigh Valley Railroad interests led by Robert H. Sayre, who recruited John Fritz -- later called "the father of the U.S. steel industry" -- as General Superintendent.11 Fritz arrived on July 5, 1860, broke ground eleven days later, and had the first blast furnace operational by January 1863. The renamed Bethlehem Iron Company rolled its first railroad rails on September 26, 1863, during the Civil War.

For two decades, rails were the primary product. Market share peaked at 11.5% of national steel rail output in 1879, but declined under pressure from Carnegie Steel and Lackawanna.12 The company's survival pivot came in 1887, when it secured the U.S. Navy's first armor plate and heavy forging contracts. John Fritz designed and built America's first heavy-forging plant between 1888 and 1892, transforming Bethlehem from a declining regional rail producer into the nation's preeminent defense contractor.13

Strategic Pivot

Bethlehem's shift from commodity rails to specialty defense products in the 1880s-1890s established the template for its next century: the company thrived when it occupied high-value niches (armor plate, structural beams, wartime production) and declined when forced to compete on commodity cost (flat-rolled steel vs. imports and mini-mills).

Joseph Wharton (founder of the Wharton School) became the largest shareholder and reorganized the business as Bethlehem Steel Company in 1899. Charles M. Schwab acquired controlling interest in 1901, and in December 1904 incorporated Bethlehem Steel Corporation -- setting the stage for its transformation into an industrial colossus.

The Charles Schwab Era and Rise to Dominance (1904-1939)¶

Charles M. Schwab was 42 years old, had just resigned as the first president of U.S. Steel after clashes with J.P. Morgan and Elbert Gary, and had acquired a struggling steelmaker valued under $9 million.14 His vision: to build "the greatest armor plate and gun factory in the world."

Schwab replaced the conservative Packer family leadership with 15 young mill executives, introduced merit-based advancement, and made a transformative $5 million bet on Henry Grey's wide-flange beam mill -- a technology U.S. Steel had rejected.15 Andrew Carnegie himself dismissed the idea: "Pioneering don't pay." Schwab's response: "If we are going bust, we will go bust big."

In January 1908, Bethlehem began producing America's first commercially successful wide-flange structural shapes. By August 1909, they were the company's biggest money makers. Bethlehem held a monopoly on wide-flange beams for 19 years, until U.S. Steel began rolling "Carnegie Beams" in 1927.16 During the 1920s, Bethlehem beams supplied an estimated 80% of New York City's skyline.

World War I transformed the company from a mid-sized producer with 1.1 million tons of capacity and 15,600 employees into an international munitions colossus. Bethlehem produced over 60% of Allied finished artillery and guns.17 Revenue surged from $135 million to $1.33 billion; annual earnings jumped from $6 million to $49 million; the stock rose from $30 to over $600.18 The legendary speculator Jesse Livermore reportedly turned $500,000 into $15 million trading Bethlehem Steel in nine months during the war boom.

Wartime profits funded a massive interwar acquisition campaign: Lackawanna Steel ($60 million, 1922), Midvale Steel and Cambria Steel (1923), McClintic-Marshall ($32 million, 1931). By 1925, capacity had reached 8.5 million tons with 60,000+ employees. McClintic-Marshall brought the structural fabrication capability that enabled Bethlehem's most iconic projects: the Golden Gate Bridge, Rockefeller Center, the Waldorf Astoria, and the U.S. Supreme Court Building.

Schwab's protege Eugene Grace ran operations as president from 1916. Grace tripled output during WWI and became the highest-paid executive in America by 1929, receiving a bonus exceeding $1.6 million on a base salary of $12,000.19 A stockholder lawsuit in 1931 demanded return of $36 million in bonuses distributed since 1911; it settled with mandatory disclosure but no repayment.

The Great Depression brought Bethlehem's first quarterly loss since 1909 in September 1931. Cumulative losses exceeded $30 million over nine quarters.20 The Nye Committee (1934-1936) held 93 hearings investigating "merchants of death" for war profiteering, though it found no conclusive evidence of conspiracy.21 Schwab died on September 18, 1939, technically bankrupt, his $7 million Manhattan mansion seized by creditors.

World War I: Arsenal of Democracy's Forge¶

Bethlehem Steel was the No. 1 munitions maker in the United States during World War I. The company produced over 60% of Allied finished artillery and guns, filled orders totaling $500 million across the conflict, and received a single British order of $135 million -- the largest in company history to that point.

Financial performance was extraordinary. Profit margins on gross sales reached 49% (1916), 58% (1917), and 46% (1918).22 Total wartime earnings of approximately $110 million represented six times the company's earnings in the nine years preceding the war. Common stock dividends reached 10% quarterly in April 1917.

The war profiteering controversies that followed would shadow the company for two decades. The Supreme Court case United States v. Bethlehem Steel Corporation (1942) concerned shipbuilding contract profits exceeding $20 million; the Court upheld the profits as not unconscionable.

Interwar Period: Expansion, Labor, and the Great Depression¶

The interwar years were defined by aggressive capacity expansion funded by wartime profits and the growing tensions between management and labor that would shape the company's cost structure for half a century.

Early labor conditions were brutal. Over 97% of the workforce worked 10+ hour days; 51% worked 12 hours or more. Blast furnace workers averaged 84-hour weeks.23 The 1910 strike (108 days, 9,000 workers) failed tactically but led to the first federal working hours law in 1912.24 The 1919 Great Steel Strike (350,000 workers nationwide) ended in complete defeat for organized labor, with two workers killed at the Bethlehem plant.

Unionization finally came during World War II mobilization. Under federal pressure, Bethlehem recognized the Steel Workers Organizing Committee (SWOC) in August 1941. The United Steelworkers of America (USWA) was formally established in May 1942.

World War II: Peak Industrial Output¶

Bethlehem Steel's contribution to the Allied war effort was staggering in scale:

| Metric | Figure |

|---|---|

| Ships built | 1,121 across 15 shipyards (most of any builder) |

| Steel produced (1940-1945) | 73.4 million tons |

| Peak employment (1943) | 283,765 |

| Airplane cylinder forgings | 70% of U.S. total |

| Warship armor plate | 25% of U.S. total |

| Cannon forgings | 33% of U.S. total |

| Sales (1945) | $1.33 billion (up from $135M pre-war) |

The Bethlehem-Fairfield Shipyard in Baltimore, built from scratch in 1941, produced 523 ships including 384 Liberty ships.25 The SS Patrick Henry, launched September 27, 1941, was the first Liberty ship built in the United States. In 1943, Grace delivered on his promise to Roosevelt of one ship per day, exceeding it by 15.26 The Fore River Shipyard in Quincy, Massachusetts surpassed all other American shipyards in tonnage delivered.

By war's end, Bethlehem was the nation's largest defense contractor -- ranking seventh among all U.S. corporations in total contract value despite being only the second-largest steel producer. The company's advantage was vertical integration: it mined the ore, smelted the steel, forged the components, and built the ships.

Seeds of Overconfidence

Grace's philosophy of relentless capacity expansion -- "I have no qualms about excess capacity. The United States will never catch up to its material needs and aspirations" -- was validated by wartime demand. But it became the strategic orthodoxy that would prove fatal when the demand environment permanently shifted.

Post-War Golden Age (1945-1970) -- Infrastructure Boom and Market Dominance¶

The quarter-century following World War II was Bethlehem Steel's zenith. The company rode a massive wave of postwar reconstruction, consumer demand, and infrastructure spending to its highest sustained production levels and profitability.

Iconic Structures Built with Bethlehem Steel¶

| Structure | Location | Completed |

|---|---|---|

| Golden Gate Bridge | San Francisco | 1937 |

| George Washington Bridge | New York | 1931 |

| Rockefeller Center | New York | 1933-1939 |

| Empire State Building | New York | 1931 |

| Chrysler Building | New York | 1930 |

| Waldorf Astoria Hotel | New York | 1931 |

| Hoover Dam | Nevada/Arizona | 1936 |

| Verrazano-Narrows Bridge | New York | 1964 |

| Madison Square Garden | New York | 1968 |

| Chase Manhattan Tower | New York | 1961 |

| U.S. Supreme Court Building | Washington, DC | 1935 |

| Chicago Merchandise Mart | Chicago | 1930 |

Production Volume and Employment¶

Financial Performance at the Peak¶

| Year | Revenue | Net Income | Raw Steel (tons) | Employees |

|---|---|---|---|---|

| 1957 | $2.6B | $190M | 19M+ | 165,000 |

| 1964 | -- | -- | 19.4M (record) | ~167,000 |

| 1966 | $2.69B | $170.9M | 21.3M | 133,000 avg |

| 1967 | $2.62B | $130.4M | 20.5M | 131,000 avg |

| 1973 | -- | $207M | 23.7M (all-time record) | -- |

| 1974 | -- | $342M (all-time record) | -- | -- |

Bethlehem ranked No. 8 on the inaugural Fortune 500 list in 1955, earning 8.2% on assets. Its president, Arthur B. Homer, was the highest-paid executive in America in 1958 ($511,249). Sparrows Point, Maryland was the world's largest steel plant with 30,000 employees and 10 blast furnaces producing 8.2 million short tons per year.

Yet the seeds of decline were planted during the golden age:

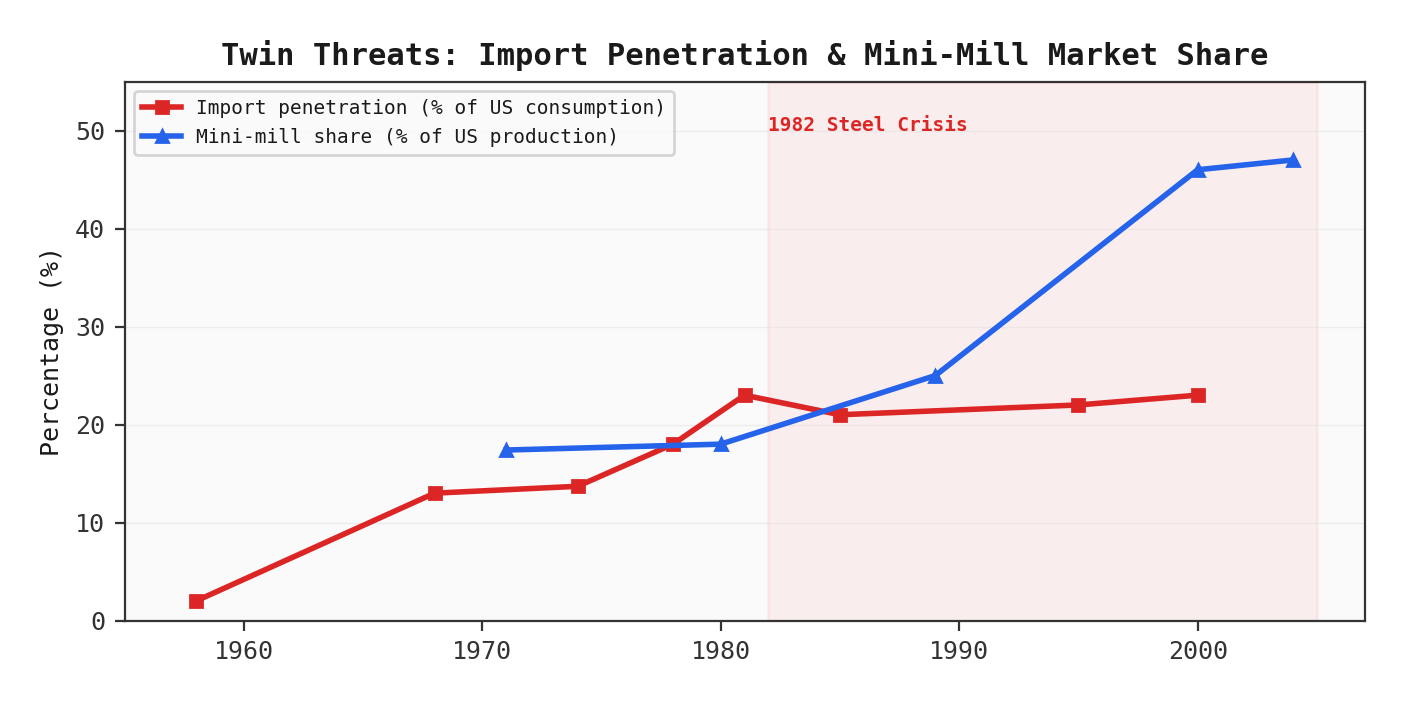

The 1959 Steel Strike was the pivotal event. Some 500,000 workers struck for 116 days.27 Steel imports surged from 2 million tons (1958) to 5 million tons (1959) and never returned to pre-strike levels. Industrial buyers discovered that Japanese steel was cheaper even after transoceanic shipping costs. In 1960, the United States imported more steel than it exported for the first time -- a structural shift, not a cyclical blip.

Technology complacency was equally devastating. Japan and Germany rebuilt their steel industries from rubble with basic oxygen furnaces and continuous casting. Bethlehem did not install its first BOF until 1964 -- a decade after Austrian commercialization.28 Worse, the company abandoned a continuous casting project at Johnstown when it was 90% complete, wasting approximately $10 million, because the plant was "physically ill-suited" -- exactly as the research committee had warned when it recommended a different site.29

Misplaced capital allocation told the story. Management spent $35 million building Martin Tower, a 21-story cruciform headquarters designed so that "innumerable vice presidents" could have corner offices. The $275 million "Big L" blast furnace at Sparrows Point added capacity. The $3 billion Homer modernization program focused on more tonnage, not better process technology. The company was investing in the last generation of steel infrastructure while competitors were building the next.

Decline and Structural Challenges (1970-1995) -- Foreign Competition, Labor Costs, and Mini-Mills¶

The Triple Competitive Squeeze¶

Three forces converged to destroy Bethlehem Steel's competitive position:

1. Japanese and Korean imports. Japan's steel production growth averaged 25% per year during the 1960s. Nippon Steel, formed in 1970, surpassed U.S. Steel as the world's largest steelmaker by 1975 with 47 million tons of annual capacity.30 POSCO, founded in 1968 with "no capital, technology, or experience," became the world's most efficient producer by the late 1980s. By the early 1980s, Japan held a $90-$100/ton cost advantage over U.S. producers, driven by modern equipment, lower wages ($8.50-$12.50/hour vs. $20/hour in the U.S.), and dramatically higher yield efficiency (89.4% vs. 71.5% in 1978).31

2. The mini-mill revolution. Ken Iverson took over a bankrupt Nuclear Corporation of America in 1965 and reinvented it as Nucor, using electric arc furnaces to melt scrap steel at a fraction of integrated mill costs.32 Nucor's first mill was built for $6 million -- a rounding error against the billions required for a blast furnace complex. The cost advantage was $50-$70/ton. In 1989, Nucor opened the world's first thin-slab casting mini-mill at Crawfordsville, Indiana, breaking integrated producers' monopoly on flat-rolled products.33 Mini-mill market share grew from 17.4% (1971) to 46% (2000) to approximately 70% today.

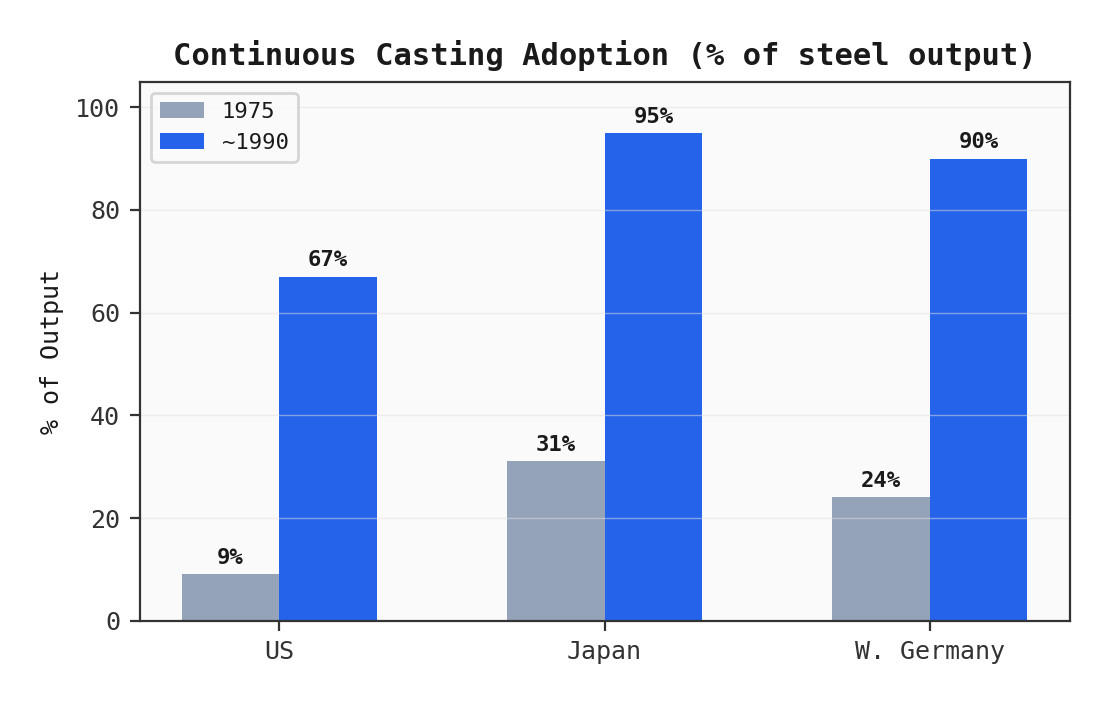

3. Bethlehem's own technology gap. The failure to adopt continuous casting was the critical error. In 1975, only 9% of U.S. steel was continuously cast versus 31% in Japan and 24% in West Germany.34 The yield gap alone -- 18 percentage points of lost efficiency -- made U.S. producers structurally uncompetitive. U.S. labor productivity improved only 16% in a decade in which Japanese productivity doubled.

Import Penetration and Mini-Mill Growth¶

| Period | Steel Imports (% of U.S. consumption) |

|---|---|

| Late 1950s | ~2% |

| Late 1960s | ~13% |

| 1974 | 13.7% |

| Late 1970s | ~18-19% |

| 1981 | ~23% (19.9M tons) |

Trade protection measures -- Voluntary Restraint Agreements (1969, 1982, 1984), the Trigger Price Mechanism (1978), and anti-dumping duties -- were repeatedly enacted but proved ineffective. VRAs were porous (non-covered countries expanded exports), and none addressed the fundamental technology and cost gaps.

The 1982 Steel Crisis¶

The 1982 recession delivered a devastating blow. U.S. steel production collapsed from 137 million tons (1973 peak) to 70 million tons by 1984. Capacity utilization fell to 49.5%. Industry-wide operating losses totaled $3.38 billion. Steel employment dropped 26% in a single year (391,000 to 289,000).

Bethlehem reported a loss of $1.5 billion in 1982 -- the largest in its history. Losses over the nine-quarter period through Q1 1984 totaled $1.7 billion.35 The company shut Lackawanna, adopted a policy of "not investing one cent more in older plants," and literally ran its aging assets into the ground before scrapping them.

Labor Costs: The Structural Trap¶

The labor cost structure that evolved through postwar pattern bargaining proved fatal:

| Metric | Figure |

|---|---|

| Average steelworker compensation (1982) | $26.29/hour (wages + benefits) |

| Premium vs. manufacturing average | 60% above (historically 30%) |

| 1973 ENA guarantee | 3% annual raises + COLA, no strike |

| Benefits package | Full healthcare (employee + retiree), SUB, 13-week sabbaticals, "30-and-out" pensions, COLA |

The 1973 Experimental Negotiating Agreement was intended to end the damaging strike cycle. Instead, it locked in cost escalation precisely when the industry needed flexibility. COLA increases were tied to national inflation, not steel industry productivity. As inflation surged in the late 1970s, compensation costs spiraled regardless of company profitability.

Cost Comparison: Bethlehem vs. Nucor¶

| Metric | Bethlehem Steel | Nucor |

|---|---|---|

| Beam production cost | Baseline | $50-75/ton cheaper |

| Profit per employee (1996) | $9,200 | $45,400 |

| Workforce for comparable tonnage | 10x | Baseline |

| Legacy cost burden | $750M/year (~$50-60/ton) | Near zero |

| Management culture | Hierarchical, class-divided | Egalitarian, performance-based |

"A Nucor minimill with half the tonnage of Sparrows Point operated with one-tenth the workers."36

Final Chapter: Bankruptcy and Liquidation (1995-2003)¶

The Last Restructuring Attempts¶

Four CEOs in twelve years tried to save the company:

| CEO | Tenure | Key Actions |

|---|---|---|

| Walter Williams | 1986-1992 | $564M Sparrows Point/Burns Harbor modernization |

| Curtis Barnette | 1992-2000 | Restructuring, plant closures, Lukens acquisition ($490M) |

| Duane Dunham | 2000-2001 | Promoted from EVP; presided over accelerating decline |

| Robert S. Miller Jr. | Sept 2001-2003 | Turnaround specialist; led Chapter 11 process |

The closures came in waves: Johnstown (1992), coke production at Sparrows Point (1993), the Bethlehem PA flagship plant (1995), coal mining operations (1991), the railroad car business (1993), shipbuilding (1997). The workforce shrank from 165,000 to 13,000.

On November 18, 1995, workers cast Blast Furnace C at the Bethlehem plant for the final time, ending 140 years of continuous steelmaking at the company's birthplace.37 Only 1,200 workers remained where 31,000 had labored during World War II.

The Lukens acquisition in 1998 ($490M plus $250M assumed debt) was the final strategic error -- a debt-financed deal at the top of the cycle, one year before the import crisis intensified and three years before bankruptcy.

The Legacy Cost Death Spiral¶

The numbers at bankruptcy were devastating:

| Liability | Amount |

|---|---|

| Unfunded pension obligations | $3.7-4.3 billion |

| Retiree healthcare (OPEB) | $3.0-3.1 billion |

| Total legacy liabilities | $7+ billion |

| Annual pension + healthcare spending | $750 million |

| Legacy cost per ton of steel shipped | $45-50 |

| Active employees | 13,000 |

| Retirees and dependents | 95,000 |

| Ratio | ~7-10 retirees per active worker |

The Arithmetic of Destruction

With 13,000 active workers supporting 95,000 retirees, Bethlehem's legacy cost burden was approximately 20 times worse than the national worker-to-Medicare-beneficiary ratio. No amount of operating efficiency could overcome $750 million in annual legacy costs on a declining revenue base.

Chapter 11 and Liquidation¶

Bethlehem Steel filed for Chapter 11 on October 15, 2001, in the Southern District of New York. The immediate triggers were the post-9/11 demand shock, record import levels, and steel prices near 20-year lows. It was the 25th American steelmaker to file since 1998.38

GE Capital provided $450 million in DIP financing. Wilbur Ross's International Steel Group bid $1.5 billion for the operating assets ($952M cash plus $700M assumed debt, net $822.6M). The bankruptcy court approved the sale on April 22, 2003. ISG got six steelmaking facilities with 10+ million tons of annual capacity. It shed all pension obligations, retiree healthcare, and environmental liabilities.

The PBGC involuntarily terminated the pension plan in December 2002 -- the largest single-employer pension takeover in the agency's 28-year history. Approximately 95,000 participants were covered, but with benefit reductions to PBGC statutory maximums.39 All retiree healthcare and life insurance benefits were terminated effective March 31, 2003. The stock was delisted from the NYSE in June 2002 after 96 years of trading.40 Shareholders received nothing.

Ross later sold ISG to Mittal Steel in 2005, which merged with Arcelor in 2006 to form ArcelorMittal. His estimated profit on the venture ranged from $118 million to $2 billion depending on the calculation method. Burns Harbor continues operating today as part of Cleveland-Cliffs.

Financial Performance Across Eras -- Revenue, Margins, and Capital Returns¶

Revenue Arc¶

| Year | Revenue | Context |

|---|---|---|

| Pre-war | $135M | Gross sales before WWII |

| 1945 | $1.33B | Wartime peak |

| 1957 | $2.6B | Peak postwar production year |

| 1966 | $2.69B | Record output (21.3M tons) |

| 1972 | $3.14B | First year above $3B |

| 1981 | $7.3B | All-time record revenue |

| 1997 | $4.63B | Last strong cyclical year |

| 2001 | $3.76B | At bankruptcy |

Profitability Trajectory¶

| Period | Net Income | Margin | Signal |

|---|---|---|---|

| WWI (1914-1918) | ~$49M avg/year | Very high (46-58% gross) | War premium |

| 1931-1933 | ($30M+ cumulative) | Deeply negative | Great Depression |

| 1957 | $190M | ~7.3% | Peak postwar |

| 1974 | $342M | ~5.7-6.2% | All-time record |

| 1977 | ($448M) | -- | First loss in 44 years |

| 1982 | ($1.5B) | -- | Steel crisis |

| 1988 | $400M+ | -- | Brief restructuring peak |

| 1997 | $280M | ~6.0% | Last strong year |

| H1 2001 | ($1.27B) | -37.3% (ttm) | Terminal |

Key Financial Ratios at Inflection Points¶

| Metric | 1957 (Peak) | 1974 (Record) | 1997 (Recovery) | 2001 (Bankruptcy) |

|---|---|---|---|---|

| Revenue | $2.6B | ~$5.5-6.0B | $4.63B | $3.76B |

| Net Income | $190M | $342M | $280M | ($1.27B) |

| Employees | 165,000 | ~100,000+ | 15,600 | 13,000 |

| Book Value/Share | Positive | Positive | Positive | ($1.29) |

| Pension Funding | Adequate | Manageable | $440M unfunded | $3.7-4.3B unfunded |

| Current Ratio | Healthy | Healthy | Improving | 0.91 |

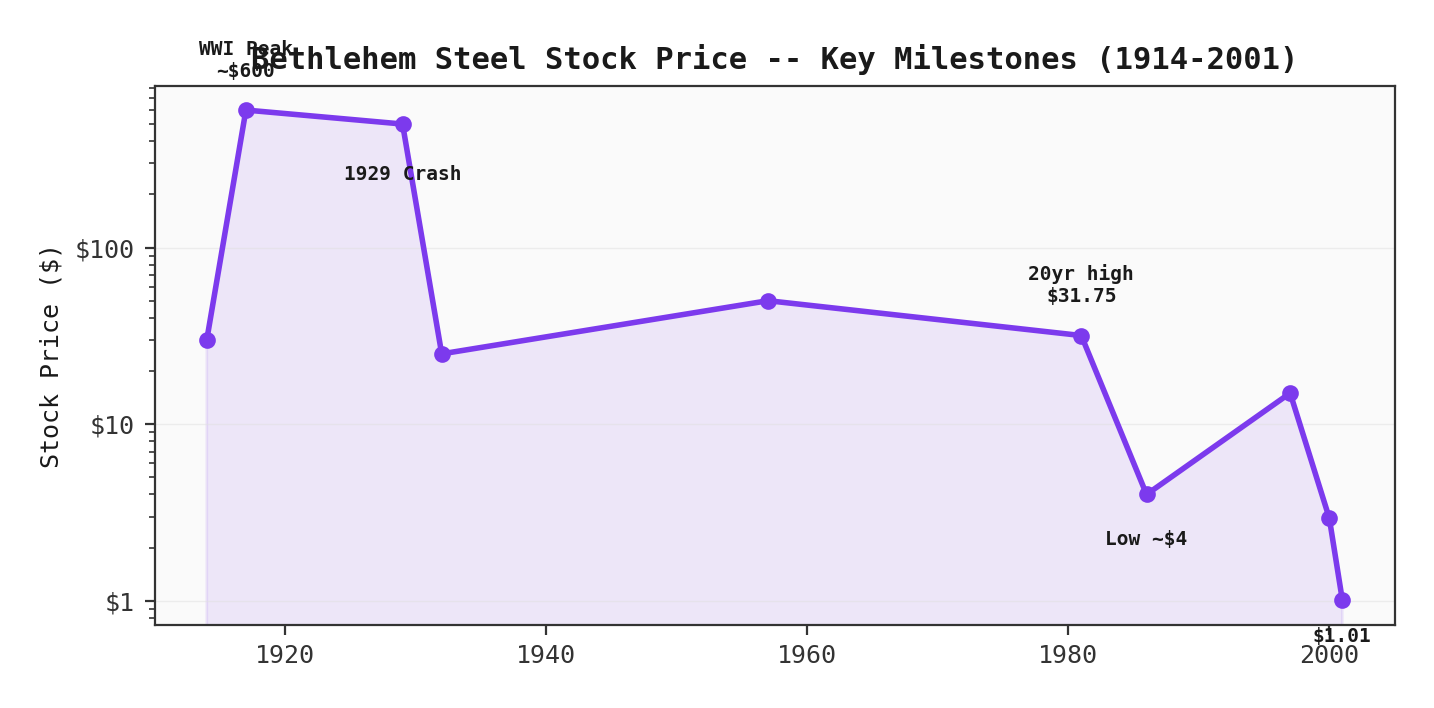

Stock Price History and Shareholder Value Analysis¶

The Full Arc¶

Bethlehem Steel traded on the NYSE under ticker "BS" from 1906 until delisting in June 2002. It was a component of the Dow Jones Industrial Average for 69 years (1928-1997) and a member of the S&P 500 from its inception in 1957 through 2000.41

| Period | Stock Price | Context |

|---|---|---|

| Pre-WWI | ~$30 | Small industrial |

| 1915-1917 | $600+ (peak ~$700) | "The war baby" -- history's original super stock |

| 1929 crash | ~95% decline | Schwab declared "never a greater stability" on October 25 |

| Late 1950s | Postwar peak | DJIA component, top-10 industrial |

| March 1981 | $31.75 | 20-year high on $7.3B revenue |

| 1986 | ~$4 | All-time modern low |

| Mid-1990s | Partial recovery | $280M earnings in 1997 |

| September 2000 | $2.94 | Fell below $3 for first time |

| August 2001 | $1.01 | Pre-bankruptcy low |

| June 2002 | Delisted | OTC penny stock, then canceled |

Dividend History¶

Bethlehem Steel paid continuous common dividends for 75 years (1916-1991), eliminated in January 1992, and never resumed. At the wartime peak, quarterly dividends reached 10% (April 1917).

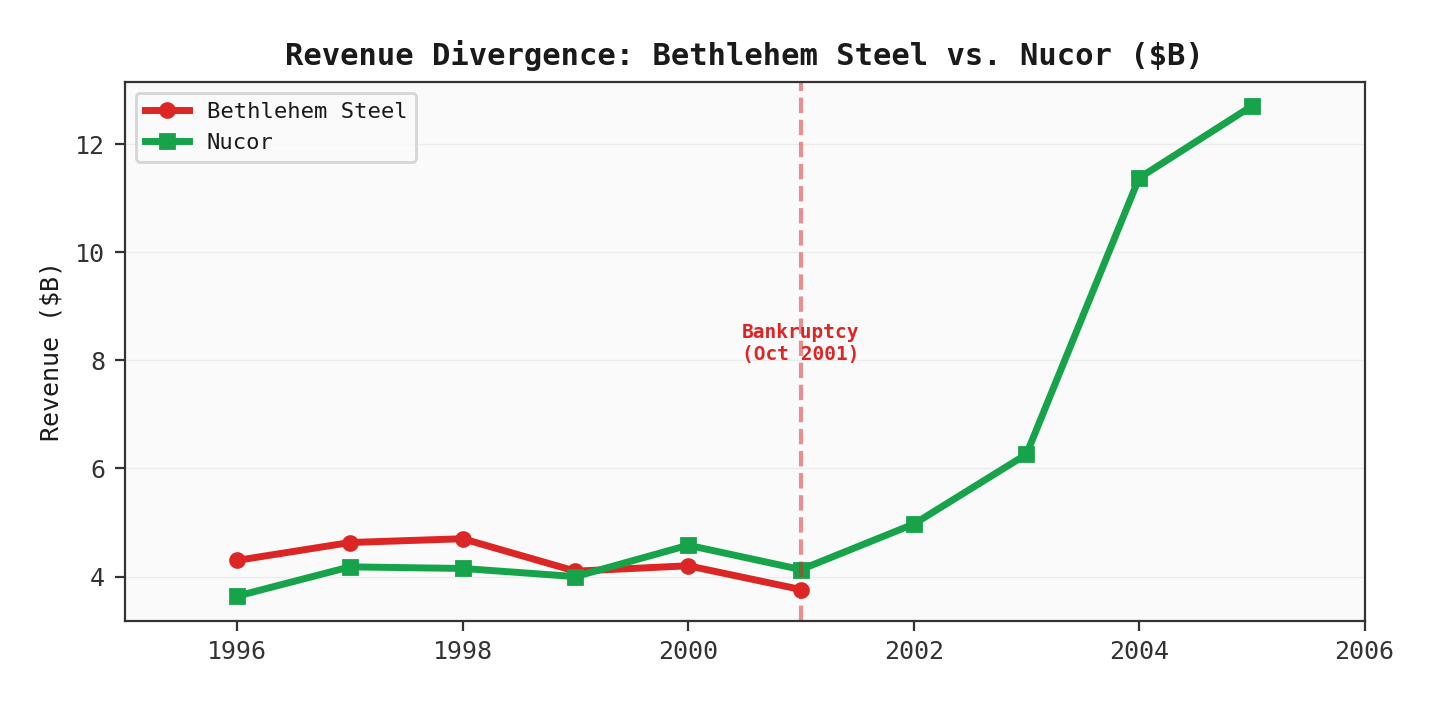

The Nucor Divergence¶

The defining comparison of American industrial history:

| Metric | Bethlehem Steel (2001) | Nucor (2001) |

|---|---|---|

| Revenue | $3.76B (bankrupt) | $4.1B (profitable) |

| Employees | ~13,000 | ~7,000 |

| Status | Chapter 11 | Profitable, growing |

| Legacy costs | $7+ billion | Near zero |

Jim Collins' research found that $1 invested in Nucor versus $1 in Bethlehem Steel diverged by over 200x. Nucor's revenue trajectory tells the story:

| Year | Nucor Revenue |

|---|---|

| 1996 | $3.64B |

| 1997 | $4.18B |

| 2000 | $4.58B |

| 2003 | $6.26B |

| 2005 | $12.70B |

By the time Bethlehem ceased to exist, Nucor was on its way to becoming America's largest steel company.

Total Return Comparison¶

A $10,000 investment in the S&P 500 in 1957 would have grown to approximately $1.5 million by 2001. The same investment in Bethlehem Steel would have been worth zero.

Legacy and Lessons -- What Bethlehem Steel Teaches About Industrial Economics¶

Why Bethlehem Steel Failed¶

The failure was not the result of a single cause but of compounding structural errors:

-

Technology complacency. The refusal to adopt BOF and continuous casting until a decade after competitors created an 18-percentage-point yield gap and permanently higher production costs. Management's instinct was to expand capacity rather than improve process -- building more of yesterday's steel mills instead of investing in tomorrow's.

-

The labor cost trap. Pattern bargaining and the ENA locked in above-market compensation regardless of individual company profitability. By the time concession bargaining began in 1986, the damage was structural: $26.29/hour total compensation, 60% above the manufacturing average, with benefits (pensions, healthcare, sabbaticals) that could not be unwound for existing workers and retirees.

-

The legacy cost death spiral. As employment shrank from 300,000 to 13,000 but pension and healthcare obligations remained for 95,000+ retirees, the per-ton burden became unsurvivable. Eugene Grace's failure to adequately fund pension plans during the profitable 1950s created a structural deficit that compounded for decades.

-

Management insularity. John Strohmeyer, the Pulitzer Prize-winning editor of Bethlehem's newspaper, documented a management culture where executives trained generations to believe "there was only one way for steel to be made: Bethlehem Steel's way." While Nucor's Ken Iverson declared "imports are a blessing... management is the problem," Bethlehem's CEO in 1983 insisted "our first, second, and third problems are imports."

-

The Lukens miscalculation. The $740 million debt-financed Lukens acquisition in 1998 -- at the top of the cycle, three years before bankruptcy -- eliminated the financial cushion that might have allowed the company to survive the 2001 downturn.

What the Collapse Created¶

Bethlehem Steel's death was not the end of American steelmaking -- it was a structural transformation:

- Wilbur Ross acquired Bethlehem's assets for net $822.6 million, stripped the legacy costs, and sold them to Mittal Steel for an estimated profit of $118 million to $2 billion.

- ArcelorMittal (formed 2006) became the world's largest steelmaker, controlling ~10% of global capacity.

- Nucor surpassed U.S. Steel to become America's largest steel company, proving the mini-mill model's superiority.

- Cleveland-Cliffs operates Burns Harbor today -- the last greenfield integrated plant Bethlehem ever built.

- SteelStacks in Bethlehem, PA, transformed the 1,800-acre former plant into one of the nation's most successful brownfield-to-arts conversions, attracting over 1 million visitors annually.

The Harvard Business School Lesson¶

HBS Case 202-088 ("The Pension Plan of Bethlehem Steel, 2001") teaches the dangers of contribution holidays when pension assets appear overfunded, asset-liability mismatch risk in pension fund management, and how legacy cost spirals can make even profitable operations unviable. The three largest PBGC losses in history all came from steel companies.

The Industrial Economics Lesson

Bethlehem Steel's 146-year arc demonstrates that competitive advantage in heavy industry is temporary unless continuously renewed through technology adoption, cost discipline, and strategic flexibility. The company's original competitive moat -- wide-flange beams, defense contracts, vertical integration -- was formidable but not self-sustaining. When the competitive landscape shifted to favor process efficiency, labor flexibility, and capital discipline, Bethlehem's moat became its prison. The blast furnaces that once made it indispensable became the infrastructure of its obsolescence.

Sources and References¶

-

FundingUniverse, "History of Bethlehem Steel Corporation"; Bethlehem Steel, Wikipedia. ↩

-

Explore PA History, "Eugene Gifford Grace Historical Marker"; Bethlehem Steel, Wikipedia. ↩

-

Construction Physics, "No Inventions; No Innovations: A History of US Steel"; Alicia Patterson Foundation, John Strohmeyer, "The Demise of Big Steel." ↩

-

Alicia Patterson Foundation, John Strohmeyer, "The Demise of Big Steel"; BLS Wage Chronology: Bethlehem Steel Corporation. ↩

-

WSWS, "Bethlehem Steel to Terminate Benefits for 95,000 Retirees" (2003); GAO-03-873T. ↩

-

Heritage Foundation, "The Steel Import Crisis"; Harvard Business School, "Nucor Revolutionizes the Steel Industry." ↩

-

PLANSPONSOR, "PBGC Takes On Its Biggest Liability Yet"; PBGC pension plan records. ↩

-

Washington Post, "ISG Offers $1.5 Billion for Bethlehem Steel Assets" (2003); International Steel Group, Wikipedia. ↩

-

Jim Collins, Good to Great; CompaniesMarketCap, Nucor Revenue Data. ↩

-

National Canal Museum, "The Beginning of Bethlehem Steel" (2021); Bethlehem Steel, Wikipedia. ↩

-

National Canal Museum, "The Beginning of Bethlehem Steel" (2021); John Fritz, Wikipedia. ↩

-

Discover America Blog, "Bethlehem Steel"; PA Center for the Book, "Bethlehem Steel: Industrial Giant." ↩

-

National Canal Museum, "Veterans Day: Bethlehem Steel's Arms and Armor" (2020); Bethlehem Steel, Wikipedia. ↩

-

Charles M. Schwab, Wikipedia; FEE, "Charles Schwab and the Steel Industry." ↩

-

WFMZ, "Bethlehem Steel's Gamble that Shaped America's Skyline"; HMDB, "The Bethlehem Beam Historical Marker." ↩

-

HMDB, "The Bethlehem Beam Historical Marker"; Company-Histories.com, "Bethlehem Steel Corporation." ↩

-

Lehigh University Environmental Initiative, "Bethlehem Steel"; David Venditta, "1918: How Bethlehem Steel Fought a War and Pestilence." ↩

-

Pennsylvania History Journal, "Bethlehem Steel"; AMP Futures Forum, "Trading History: Bethlehem Steel." ↩

-

Eugene Grace, Wikipedia; FundingUniverse, "History of Bethlehem Steel Corporation." ↩

-

FundingUniverse, "History of Bethlehem Steel Corporation." ↩

-

EBSCO Research Starters, "Nye Committee"; U.S. Senate, "Merchants of Death." ↩

-

Pennsylvania History Journal, "Bethlehem Steel" (wartime profit margin data). ↩

-

WFMZ, "History's Headlines: The Great Bethlehem Steel Strike of 1910"; Roots & Wings Research, "Hot, Loud, and Dangerous." ↩

-

National Canal Museum, "The 1910 Bethlehem Steel Strike." ↩

-

Wikipedia, "Bethlehem Fairfield Shipyard"; Maryland 400, "Bethlehem-Fairfield Shipyard Builds the First Liberty Ship." ↩

-

Explore PA History, "Eugene Gifford Grace Historical Marker"; Bethlehem Steel, Wikipedia. ↩

-

Steel strike of 1959, Wikipedia; Encyclopedia.com, "Bethlehem Steel Corp." ↩

-

Basic Oxygen Steelmaking, Wikipedia; Construction Physics, "No Inventions; No Innovations." ↩

-

Alicia Patterson Foundation, John Strohmeyer, "The Demise of Big Steel." ↩

-

Britannica, "Nippon Steel Corporation"; Nikkei Asia, "US Steel Production Exceeds Japan's." ↩

-

Heritage Foundation, "The Steel Import Crisis"; Princeton/OTA, Continuous Casting Technology Assessment (1979). ↩

-

Charlotte Museum of History, "Ken Iverson and Nucor Corporation"; Nucor, Wikipedia. ↩

-

Harvard Business School, "Nucor Revolutionizes the Steel Industry"; Congressional Research Service, R47107. ↩

-

Construction Physics, "No Inventions; No Innovations: A History of US Steel." ↩

-

Alicia Patterson Foundation, John Strohmeyer, "The Demise of Big Steel"; Bethlehem Steel, Wikipedia. ↩

-

Baltimore Sun, "No Respite Is in Sight for Struggling Giant" (1996). ↩

-

Seattle Times, "Bethlehem Steel Extinguishes Furnaces at Flagship Plant" (1995); Lehigh Preserve, "The Final Years." ↩

-

CNN Money, "Bethlehem Steel Files for Bankruptcy" (2001); Baltimore Sun (2001). ↩

-

PLANSPONSOR, "PBGC Takes On Its Biggest Liability Yet"; Business Insurance, "PBGC Terminates Bethlehem Steel Pension Plan." ↩

-

Slate, "Bethlehem Steel, from A-list to Delist" (2002). ↩

-

Dogs of the Dow, "DJIA Additions and Deletions"; Slate, "Bethlehem Steel, from A-list to Delist" (2002). ↩